The Trader's Mind: Path to Profitability"

The Trader's Mind: Path to Profitability"

Exploring the Role of Intelligence, Personality Traits, and Self-Control in Trading and Performance-Based Jobs

Being a trader is great! The markets are open to all, eliminating the need for extensive university education, entrance exams, and getting a student loan (if you're from the US). Even traditional apprenticeships are unnecessary. Moreover, with the advent of Prop firms, even undercapitalisation is an easier barrier to overcome compared to a few years ago.

Yet the numbers are precise: the proportion of private traders that manage to conclude the year profitably, factoring in commissions, data feeds, trading platforms, and other expenses, ranges from 3% to 5% [1], contingent upon the sample size examined.

In contrast, when it comes to institutional traders, AKA those who are actively employed by entities such as banks and pension funds, the success rate rises to 50%.

CAR = Cumulative Abnormal Return (market-adjusted)The graph shows how the returns differ from expectations for the stocks bought minus the stocks sold by institutions and individuals, weighted by the net value of the stocks bought and sold. The stocks that are net bought by institutions exceed those that are net sold by four percentage points after 140 trading days.

Source: "Just How Much Do Individual Investors Lose by Trading?" Brad M. Barber, Yi-Tsung Lee, Yu-Jane Liu, and Terrance Odean, The Review of Financial Studies, Volume 22, Number 2, 2009. © Oxford University Press

What is the reason behind the success rate difference between independent and institutional traders?

The answer is straightforward: firstly, 'institutional' traders are chosen through a rigorous skill validation process. They are then trained to carry out operations that leverage a proprietary statistical edge grounded in highly favourable execution conditions, such as reduced commissions, priority channels for news updates, and other tools, sadly unavailable to the 'retail' traders. Furthermore, they receive ongoing mentorship from more seasoned professionals.

A context that strikes a balance between retail and institutional settings is that of hedge funds.

Traders backed by a private hedge fund typically have a lower success rate than their institutional counterparts but significantly higher than independent traders.

This is because, while they do not possess the proprietary edge offered by an institution, they often have to craft a profitable strategy semi-independently. Nevertheless, they benefit from potential mentorship provided by the fund's veterans.

Moreover, like 'institutional' traders, they are usually chosen through a specific series of tests designed to analyse the candidate's background and personality traits.

This is one of the topics explored by Brent Donnelly in his book 'Alpha Trader', which compiles various statistics related to the themes mentioned above in its initial part.

The critical question then arises: how can private traders leverage this information? What cognitive-behavioural characteristics differentiate a profitable trader from the remaining 95%?

Does Intelligence play a role?

'Intelligence' is a broad term that can refer to diverse factors depending on the context.

For the sake of this article, it should be narrowed down to 'Intelligence Quotient' (IQ), which refers to the capacity for 'pattern recognition' as measured by tests validated by statistical norms used in the clinical field.

High IQs are associated with a propensity to visualise and grasp progressively more complex mathematical-statistical concepts. Useless to say that statistical knowledge is precious in trading as it forms the foundation of Risk Management.

Are there statistics correlating IQ with trading profitability?

The answer is negative. However, it is possible to analyse the relationship between IQ and income, as well as IQ and academic performance.

Entrepreneurial endeavours, just like independent trading, are correlated with much higher-than-average incomes (when it goes right) and with a high failure rate, therefore, the likelihood of finishing the year in the black.

For instance, updated 2023 statistics in the world of self-publishing indicate that 90% of indie authors sell fewer than 100 copies a year [2], and only just over 2% manage to exceed 5000 copies sold [3]. This picture closely mirrors the success rate of independent traders!

The relationship between IQ and academic performance enables us to gauge whether IQ genuinely plays a role in endeavours that test problem-solving skills, comprehension of new concepts, and memorisation.

As evidenced by the two statistical illustrations below, a slightly positive correlation has recently emerged between IQ and income, as well as between IQ and academic performance.

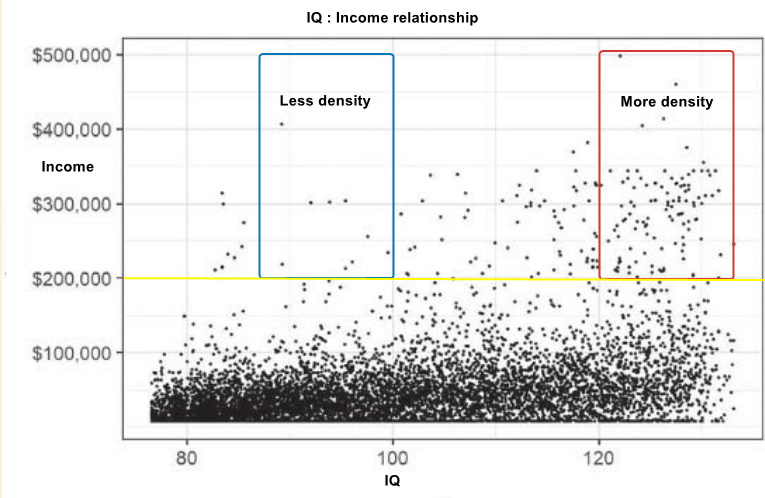

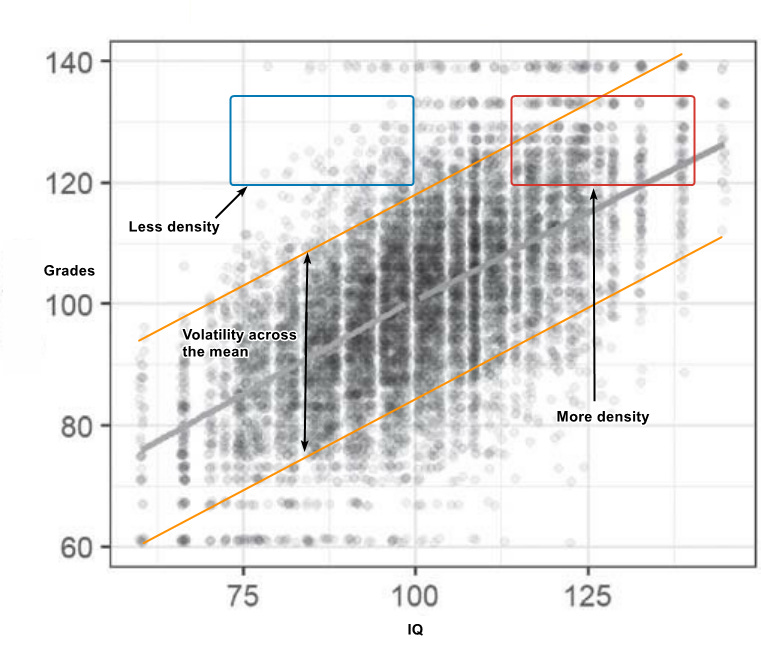

Stats from Jonatan Pallesen https://jsmp.dk/posts/2019-06-16-talebiq/The first graph illustrates the distribution of IQ (X-axis) and annual income (Y-axis) for a given population sample. The second graph provides a similar picture of IQ (X-axis) related to the average grades in school (Y-axis).

In both cases, the red quadrant (high IQ + annual income above 200k USD; or high IQ + high school return) shows a more dense concentration of matches compared to the blue one (medium/low IQ + annual income above 200k; medium/low IQ + high school return).

Notably, the densest match concentration in the income graph remains below 50k USD of annual income across the X-axis. This suggests that while a correlation exists between high IQ and above-average yearly income, most high-IQ individuals earn below 50k USD per year, similar to their medium-low IQ counterparts.

The picture is slightly more evident in the IQ and academic performance graph, where the 'intelligence' factor seems to impact academic performance more significantly than income. Nonetheless, significant volatility is observable around the traced average.

There are plenty of high-IQ individuals with poor academic performance, just as there are medium-low-IQ individuals with high academic performance.

School performance proves to be a more reliable indicator than IQ to personal "success" and annual income [4].

This is because Intelligence is just one of the many factors that can influence a student's performance. Work ethic, discipline, and self-control play an equivalent, if not superior, role.

An individual's personality can negate the benefits of a high IQ or, alternatively, augment them, thereby aiding the acquisition of necessary skills for success in the chosen field, including trading.

So, which personality traits have the most significant impact on trading and any other performance-based activity?

Liking the article so far? Consider subscribing to this newsletter, and don’t forget to share it with your friends!

The Impact of Conscientiousness

Conscientiousness is a personality trait associated with an individual's inclination to organise their life and work efficiently and methodically.

A highly conscientious individual is proficient in creating to-do lists and punctual for appointments. Conversely, low conscientiousness characterises a work style largely dependent on improvisation, to put it nicely.

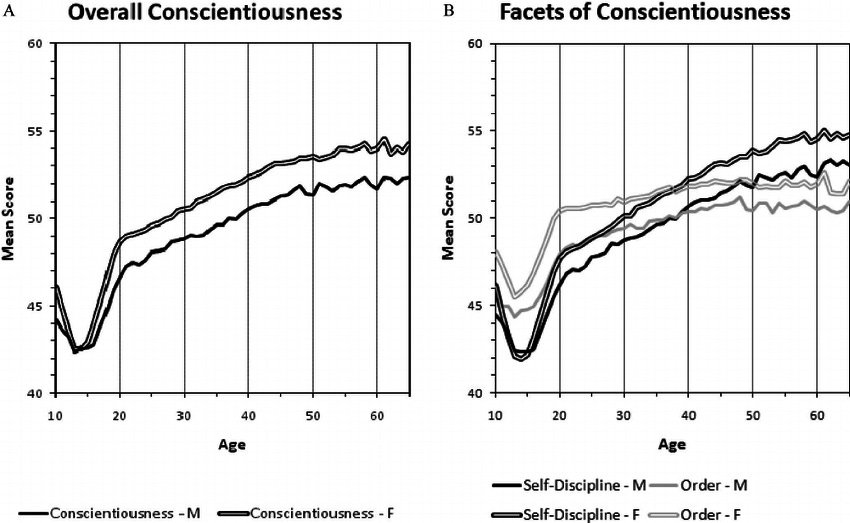

While other personality traits, such as introversion or extroversion, tend to remain stable throughout life, conscientiousness undergoes a continuous transformation as an individual ages. In fact, it reaches its minimum during adolescence, then rises linearly after age 20, generally peaking after 50 years of age [5] .

Averages for general Conscientiousness (A) and for its facets (B), based on age and gender. Single lines show averages for males, and double lines show averages for females. -- Soto, Christopher & John, Oliver & Gosling, Samuel & Potter, Jeff. (2011). Age Differences in Personality Traits From 10 to 65: Big Five Domains and Facets in a Large Cross-Sectional Sample. Journal of Personality and Social Psychology. 100. 330-348. 10.1037/a0021717. A high degree of conscientiousness is correlated to strong "self-control". Self-control is the most critical behavioural factor characterising successful traders [6], considering the significance of risk management and the ease with which an account can be liquidated during an impulsive bout of 'revenge trading'.

Self-control enables traders to methodically execute a strategy without deviating from predetermined triggers or sizing. Successful traders do not attempt to impose their bias on the markets. They patiently wait for the opportune moment, and when it arises, they act according to their established plan.

Vulnerabilities

You, on your third failed Prop challenge attempt in a row.

A personality trait that detrimentally influences traders is a predisposition towards neurotic tendencies such as irritability, anxiety, and depression.

Irritability erodes "self-control", leading the trader towards revenge trading and impulsive decisions that deviate from the plan, or in other words, from the pre-established trading strategy.

On the other hand, anxiety also hinders the accurate execution of the trading plan. Still, in this case, the trader refrains from taking risks despite clear operational setup signals showing up on the chart.

Lastly, depression subjects the trader to negative self-talk, undermining confidence in their capabilities, therefore obstructing the correct analysis of their operations with a rational mindset.

Self-assessment and Personal Improvement

Suppose a trader identifies themselves as a neurotic individual with low levels of conscientiousness. Can they change their behaviour, or are they doomed to a predetermined path of constant failure?

Conscientiousness levels can be improved by consistently employing the following behavioural strategies in daily life:

The Leverage of Friction

Everyone tends to postpone activities that could positively impact health or personal growth because they usually demand a fair amount of effort.

In contrast, the immediate dopamine surge from an hour of compulsive TikTok scrolling never faces procrastination since it offers instant gratification without requiring any effort in exchange.

Carrying out an effortful activity depletes an individual's "motivation" reserves, which are not infinite.

As James Clear highlights in Atomic Habits, the more intense the friction between the individual and the task initiation, the more motivation is needed to get off the couch and begin working on the said task.

Let's see a practical example:

If my goal is to run every day for 20 minutes, but I think it's reasonable to keep my running shoes in their box, conveniently stashed on the third shelf of my closet, behind a mountain of clutter and boxes, I am actively sabotaging my chances of successfully maintaining my goal.

Every time I intend to go running, I must embark beforehand on a tiresome treasure hunt to find the shoes and that just to put myself in a position to start the planned activity!

The rather obvious outcome is that, on the first occasion when my intrinsic motivation to perform such activity is particularly low, the likelihood of forgoing the run, opting instead for the "TikTok on the couch" alternative, will be very high.

This is an instance of "intense friction" that, in this case, obstructs the long-term sustainability of a health-benefiting activity.

If my goal is to lose weight, but I can't resist the delightful chocolate biscuits that I persistently buy every weekend and then store in a readily accessible bowl in the kitchen, at the first lapse in my motivation to reduce daily caloric intake, I will inevitably end up grabbing a generous handful of biscuits.

This is an instance of "low friction", which facilitates impulsive behaviour with a detrimental effect on health.

The solution? Simple: decrease the friction for performing the beneficial activity by placing the running shoes directly next to the entrance door, and simultaneously, increase the friction between you and the execution of the detrimental habit, perhaps by not keeping biscuits at home at all, enforcing a rule to consume them only outside the home.

This way, I would be compelled to make an effort that would truly test my desire to eat those biscuits since I have to get to the store to grab them. And it wouldn't be a bad idea to fill that kitchen bowl with seasonal fruit instead.

The trick is to utilise friction to your advantage to make "negative" activities for health and/or personal growth harder to carry out and, conversely, to make "positive" actions easier to execute.

Zeigarnik Effect and Micro-goals

Is it easier to write a 200-page book or a 1500-word post?

A 200-page book equates to about 60,000 words, which can be broken down into 40 posts of 1500 words each.

Essentially, a book is an aggregation of several chapters posts.

When facing any activity that demands active engagement, the human brain preemptively measures the anticipated amount of effort.

Setting the goal of writing an entire book can easily provoke procrastination, resulting in straying from the predetermined plan due to the apparent "immensity" of the task at hand.

On the other hand, committing to write a 1500-word post seems more mentally manageable, as does allocating 15 minutes daily to journaling your trades instead of dedicating the entire weekend to retrospectively cataloguing the week's trades.

Once the task is divided into more mentally digestible parts, thus appearing feasible without causing burnout at the mere thought, there's a simple strategy to maximise the probability of completing the set goal: commit to accomplishing only the first step, the initiation of the task, each day.

Referring back to the example of writing 1500-word posts, the first step is to open the text editor and review the list of topics.

The first step for the trader's journaling goal involves opening your journaling software or Excel and the folder containing screenshots of your trades.

The remaining part of the task will come naturally, and even if you halt the execution of the task at that moment - for whatever reason - you are likely to resume it later.

This is due to the so-called "Zeigarnik effect," [7] a phenomenon described by Russian psychologist Bluma Zeigarnik in 1920 that demonstrates people's propensity to recall interrupted or incomplete tasks better than those completed already.

The recipe for shifting towards a more conscientious approach to managing work involves fragmenting the ultimate goal into numerous micro-tasks and concentrating solely on them.

Therefore, by effectively utilising the Zeigarnik effect and committing 1500 words a week to predetermined topics, the seemingly gargantuan project of a 60,000-word book will be accomplished in less than a year.

Managing Limiting Factors

Anxiety, depression, irritability: kryptonite for traders. If you find yourself prone to these types of neuroses, does that make you inherently unsuitable for trading?

While this can certainly be a significant vulnerability, there are evidence-based practices such as mindfulness and cognitive behavioural therapy that can mitigate the negative impact of these traits on your trading performance and general life quality. These methods can be especially effective when aided by a professional.

One particularly effective technique borrowed from cognitive behavioural therapy is "Episodic Future Thinking" (ETF). This practice involves visualising specific and positive personal future experiences, projecting oneself into a hypothetical future scenario.

As a trader, you might visualise yourself feeling satisfied and serene during a successful trading streak. This vision should be vivid and visceral, so realistic and gratifying that it stimulates the most primitive part of our brain: the reptilian brain.

Satisfying the cravings of the reptilian brain with your most enticing desires is a successful strategy to limit the potential damage that your inner beast could inflict on your real life and your PnL.

"Don't follow your instinct, Luke."

In the financial world, references to "gut feelings" are common, but is instinct really a determining factor for a trader's success?

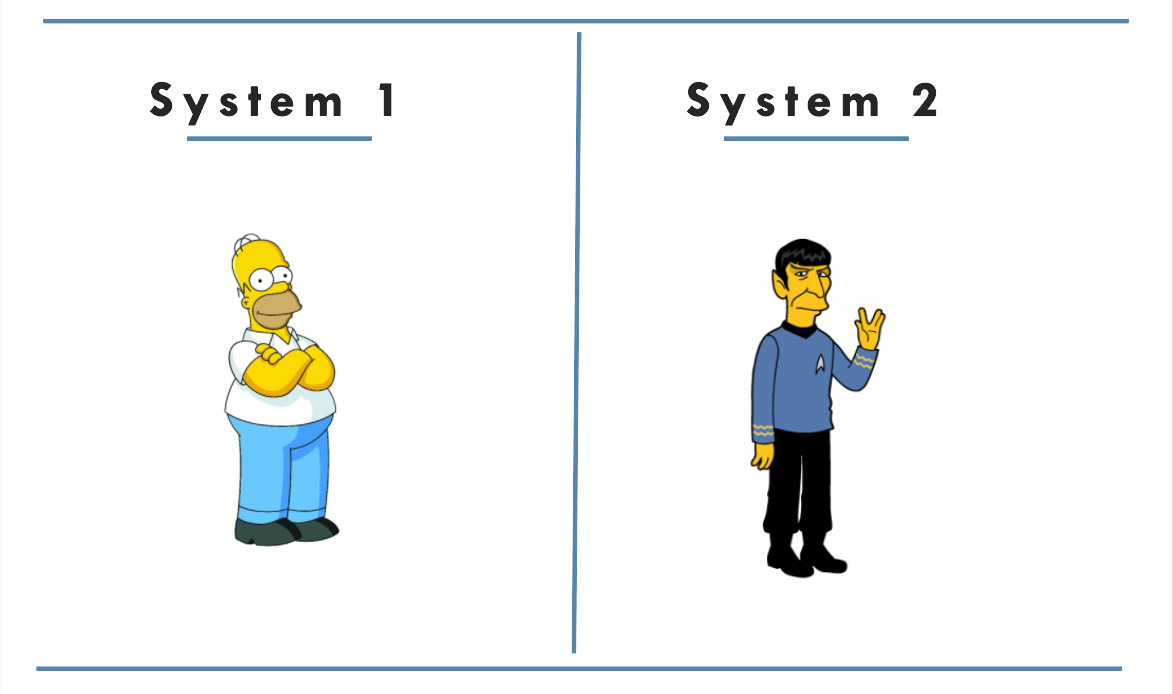

In the previous section, I mentioned the so-called "reptilian brain." Let's dive deeper into our cognitive systems based on the classification provided by Nobel Prize-winning psychologist Daniel Kahneman in his book "Thinking, Fast and Slow" [8]:

System 1: the reptilian brain, i.e., the parts of the brain responsible for instinct. It operates rapidly, requires no conscious effort, and can process vast amounts of data. However, it sacrifices accuracy for speed, relying on primitive associations and numerous cognitive shortcuts.

System 2: the rational and conscious part of the brain, which we use for logical and mathematical processes. It processes information slower than System 1 and requires significantly more effort, but it enables us to exercise rational thinking.

The two systems are linked. System 1 acts as an environmental filter, passing on to System 2 the information that requires more complex processing.

For example, when your stomach is empty, System 1 triggers a sense of hunger in your brain, making you want to eat whatever's within reach. System 2, on the other hand, allows you to choose more wisely what to eat, considering, for example, that since you're on a diet (because you likely are), maybe a slice of cheesecake isn't the best choice to satisfy your immediate craving.

In trading, those who let System 1 dominate often fall prey to FOMO (Fear Of Missing Out). They might impulsively open a position—often with reckless contract sizes—perhaps in response to a news release or as a form of revenge trading.

Is Spock Cut Out to Be a Successful Trader?

The book "Alpha Trader" examines an extensive collection of psychological studies done on traders from various hedge funds.

These studies reveal that rationality is the trait that most significantly impacts the success of traders [9].

The so-called rationality quotient (RQ) is more relevant to trading performance within a large sample of individuals than the intelligence quotient (IQ).

Conversely, overconfidence is the behavioural trait that most accurately predicts failure in trading activities and in any performance-critical task, such as sports or entrepreneurship.

Understandably, rational reasoning aligns directly with System 2, whereas an excessive belief in one's abilities is a consequence of instinctive behaviour, thereby relating to System 1.

Although IQ and RQ are positively correlated, particularly high IQ levels do not make one immune to the development of "confirmation bias."

Just like normal individuals, people who are particularly gifted cognitively are still potential prey to System 1, which can lead these subjects to develop excessive confidence in their abilities or, on the contrary, the opposite phenomenon: an underestimate of their abilities.

Even though IQ and RQ correlate positively, having exceptionally high IQ levels does not act as a shield from the development of "confirmation bias." Much like average individuals, cognitively gifted individuals can still fall prey to System 1. And confirmation bias can lead these individuals to develop either excessive confidence in their abilities or, conversely, an underestimation (impostor syndrome).

Both situations indicate a dominance of System 1 over System 2, which needs to be promptly identified for the trader to objectively and rationally evaluate their trading system through a rationalisation process.

Testing Rationality

The rationality quotient can be assessed through the Cognitive Reflection Test (CRT) [10], which consists of three simple questions:

A bat and a ball cost a total of $1.10. The bat costs $1.00 more than the ball. How much does the ball cost?

If 5 machines take 5 minutes to produce 5 widgets, how long would 100 machines take to make 100 widgets?

In a lake, there is a patch of lily pads. Every day, this patch doubles in size. If it takes 48 days for the patch to cover the entire lake, how long would it take for it to cover half of the lake?

If you answered 10 cents, 100 minutes, and 24 days, your System 1 dominates over System 2, making you susceptible to instinctive associations.

If you answered 5 cents, 5 minutes, and 47 days instead, you display Spock-like rationality.

Dominating System 1 in Trading

So, you're System 1 dominant and can't resist opening a position driven by your gut feeling, perhaps due to recent news. What's the solution? The key is to react rationally right after giving in to the impulse.

You've opened the position—excellent. Now, take a step back and analyse your decision using System 2:

Is the trading idea logically sound, or upon deeper reflection, is there no justifiable reason to keep the trade open?

If you find a logical foundation in the trade after its initiation, preferably aligned with your trading system's rules, that's good. You can maintain the position.

However, if, through rational thinking, you discover that the trade lacks any logical basis, you must immediately close the position. Patiently wait for the next setup to appear, and don't delay closing the position until it breaks even. Just scratch it!

In trading, as in entrepreneurship, limiting damage using a rational approach is crucial. This is the foundation for survival in any performance-dependent occupation.

Psychology of Limit Orders and Market Orders

In your view, are traders who use limit orders statistically more profitable, or do those who enter the market aggressively using market orders fare better?

In a 2008 study titled "Trader Personality and Trader Performance: a Framework and Financial Market Experiment" by van Witteloostuijn, A.; Muehlfeld, K.S., it was found that traders with lower trading frequency, who primarily use limit orders, tend to outperform those using market orders [11].

Does this suggest that simply changing the type of execution can lead to profitability? Not necessarily. However, placing a limit order and waiting for the corresponding fill indicates the dominance of System 2. The trader is patient and confident in their analysis and trusts their statistical findings.

On the other hand, entering at market price typically signifies impulsiveness unless such a practice is backed by a statistical model and thus part of a rational decision-making process.

TL:DR

The Intelligence Quotient (IQ) slightly positively impacts but isn't decisive in acquiring the skills necessary to become profitable traders.

The Rationality Quotient (RQ) is most influential in achieving success in the trading profession.

Conscientiousness, the ability to organise effectively, is a vital trait for every professional trader. This trait can be enhanced through managing decisional friction, exploiting the Zeigarnik effect, and implementing micro-goals.

Allowing System 1 (the reptilian brain) to dominate in trading leads to succumbing to FOMO and revenge trading, rendering the application of a carefully considered trading strategy impossible.

System 1 can be managed through Episodic Future Thinking (EFT).

Closing words

Being a trader is great, yes. But only for some.

Unrestricted market access is a pitfall for those unable to approach it rationally. Some individuals are better predisposed to cultivate the correct mindset to survive in the financial jungle.

In "Alpha Trader"—a book I highly recommend for a deeper understanding of the topics discussed in this article—Brent Donnelly offers the following formula:

Success in trading = rational thinking + IQ + self-control - overconfidence.

Anyway, as trading requires continuous application of System 2, prepare for a substantial dose of effort.

This article is sponsored by SaviusLLC, the only prop firm with fair rules for swing traders and supporting EUREX symbols

If you liked this article, you might also like these previous ones:

Suggested readings:

Menno Henselmans: “The Science of Self-Control”

Brent Donnelly: “Alpha Trader”

Daniel Kahneman: "Thinking, Fast and Slow"

James Clear: “Atomic Habits”

References

[1] What's the Day Trading Success Rate? The Thorough Answer | Invezz

[2] Self-published Books & Authors Sales Statistics [2023] – WordsRated

[3] A Bookselling Tail (publishersweekly.com)

[4]True grit and genetics: predicting academic achievement from personality - PMC (nih.gov)

[6] (PDF) The Impact of Self-Control on Investment Decisions (researchgate.net)

[7] Zeigarnik effect - Wikipedia

[8] Thinking, Fast and Slow - Wikipedia

[10] Cognitive reflection test - Wikipedia

[11] Trader personality and trading performance: A framework and financial market experiment (uu.nl)